Pricing

To better asses a tax position we offer an intake service: a meeting of one hour for which no fee will be invoiced.

Our services are based on an hourly rate multiplied by the time spent. The rate is € 150,- per hour. For some services we are able to work with fixed fees. On this page you find an overview of both (examples) of our hourly rate services and fixed fees services.

Dutch market – hourly rate

Advice on:

- complex income tax issues;

- residency;

- handling requests for information from tax authorities;

- estate planning;

- civil law.

Dutch market – fixed fee*

Service | Rate |

|---|---|

Income tax return | € 495,- |

Request to average out 3 year income | € 395,- |

Prepare provisional tax refund | € 195,- |

File extension for submitting income tax return | € 75,- |

30% ruling | € 695,- |

Administration and VAT | t.b.d.** |

Provide postal address service for tax letters (annual fee) | € 95,- |

Request refund dividend withholding tax – Various countries | t.b.d.** |

US market – fixed fee*

Service | Rate |

|---|---|

Income tax return – Federal | t.b.d.** |

Income tax return – State | t.b.d.** |

Request extension filing income tax return | € 75,- |

UK market – fixed fee*

Service | Rate |

|---|---|

Income tax return | € 795,- |

All prices are ex. 21% VAT.

References:

*Pricing is based on cases of average complexity.

**To be discussed: the pricing varies to the extent complexity of the case.

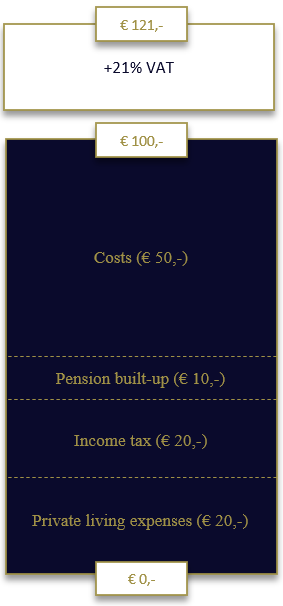

Pricing built up

Our goals is to help athletes. One of the things we find important is to be transparent. We want to reflect this in, amongst other things, explaining our pricing structure. As an example we breakdown one hour of paid work (€ 100,-). (Note that not all worked hours are paid. In general half or the worked hours are actually billed). Numbers are based on the 2021 annual report.

From every € 100,- income, the first € 50,- are costs that need to be deducted. Example of costs are: rent office space, office needs (copy costs, paper etc.), write off computer and other assets, phone costs, insurance, IT (programs, website, hosting etc.), tax law/ literature subscriptions, permanent education costs, marketing, acquisition etc. Then € 10,- is taken of for pension built-up, after which € 40,- results. On this amount 50% income tax is paid.

At the bottom-line, from every € 100,-, € 20,- can be used for private life matters (rent, utilities, food, clothing etc.).